|

M.E.T.T.S. - Consulting Engineers > Opinion Pieces & Conference Presentations > The Survival of the Extractive Industries (EIs) Through and Beyond the COVID Crisis

The Survival of the Extractive Industries (EIs) Through and Beyond the COVID Crisis

The EIs' Likely Approach and Options for Economic Harm Minimisation and Future Growth

Dr. Michael C. Clarke

CPEng, FIEAust, APEC Engineer, IntPE (Aus), FAusIMM, RPEQ (mining & chemical)

M.E.T.T.S. P/L, Consulting Engineer, Infrastructure Developing & Resource Management

Email: metts[at]metts.com.au

Preamble

The AusIMM has been looking for ways to reduce (or even remove) shortfalls in the professional ranks that are apparent in EIs. Having "lost" professionals that are interested to resuming their association with the EIs and enticing graduates with similar qualifications come into the EIs after a short "re-education" programme.

The simple concepts suggested above are now however complicated thanks to COVID-19 adding additional complexity to what is an already multi-faceted task. The simple concepts will be tested as COVID causes professionals to leave the remote EI sites but creates a potential replacement workforce from those locked-out of other industries by the COVID Recession that may develop into a Depression.

In economics terms the EIs are the sellers of mostly raw or marginally transformed products, products that must find customers for purchase and off-take. During post COVID recovery, nations and industries that are least damaged and can go back into reliable production in tandem (ahead) of customers demand for supplies, will be winners. Being a trusted supplier will be important in a world in social. Political and financial mayhem.

Looking at the challenges from the AusIMM perspective with its concentration on professionals the continuance of being part of finding engineers, applied scientists, and managers (with a combination of technical, financial as well as management skills) is a very worthwhile activity, however finding and retaining technicians and semi-skilled people in greater numbers is crucial for the EIs. Creating and maintaining stability in the skilled workforce that includes social security as well as reasonable work security is required for the EIs. Practices such as FIFO should be sent to the bin-of-history for most people involved in the EIs. Creating security in remote communities will be important in seeking and retaining all classes of a skilled workforce; however some professionals and technicians, working as inhouse, tied or independent consultants could still be FIFO -- this would help cover skills shortages in the upper echelons of the professional and senior technical workforce.

On the international front the apparent veracity of the of the Australian COVID-19 reporting and tracking system will be reassuring to buyers of Australian products in that there is now, and presumably into the future, trust in what we are presenting as being our capabilities in "delivering the goods" to purchasers and off-takers. If COVID-19 mutates and produces strains, develops strains that are resistant to vaccines, finds a continuing zoological vector, develops the ability to permanently injure human organs (e.g. the heart, liver and/or kidneys) and/or develops only short-lived immunity post infection, then a seasonal wave of epidemics (like the season flu epidemics) can be expected and will cause ongoing harm. It can be noted here that Government is relying less on the notion of having a vaccine in "eighteen months" than having drugs that will counter the infection once caught. In other words if Australia can moderate the effect of future COVID epidemics, then we will have an advantage over other parts of the world, such as Africa, Latin America and South Asia, who have only basic health monitoring systems.

So, Australia and its EIs may have advantages in a post COVID world.

Introduction

The education and training of professionals, lower management and technicians and thence the retention of those people by the EIs through their productive lives is a necessary goal for the EIs. Likewise the training and retention of unskilled personnel who through the workplace (and skills training institutions) have become semi-skilled, is also very important. The AusIMM has a specific charter to guide, support and assist with future planning of the professional end of the workforce; this paper is primarily concerned with the professional end of the workforce spectrum.

The boom-bust nature of the EIs and the COVID outbreak

The on-coming recession (potentially developing into a depression) is seeing industry/production crash with international and domestic buyers of EI products withdrawing from the market; the reduction in petroleum demand being one example. The outbreak is also seeing the supply of imported machinery, domestic goods, food products, apparel etc "dry-up"; this will have a major effect on EI workforce (and indeed the entire nation will be crippled by this initially supply led recession).

Having become a nation of raw materials exporters with relative low (and continuously decreasing production of elaborately transformed manufactures) that needs imports to survive we are in a parlous state; the policy of living off raw materials exports, having an ever-expanding services industry and public sector, and assuming that supply of essential goods is being truly tested. The COVID outbreak has destroyed the myth of there always being a balance between raw materials returns from sales versus the outward cash-flow for imported manufactures; the other potential challenge to that myth is upheaval from an East-Asian war (that still could come!).

The EIs in the greater scheme of economics, society and national well-being

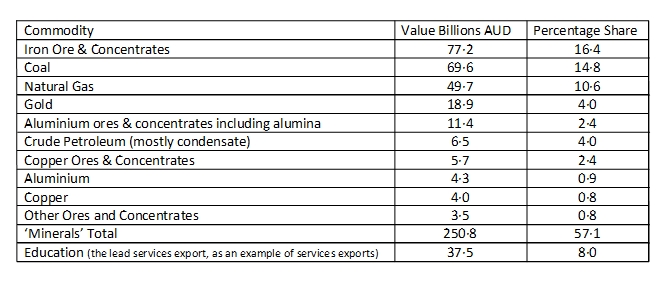

The EIs are very important to the world's economics, society's performance and the well-being of the global population. Their raw and semi-processed value is presented below.

Table 1: Export "Mineral" Value, Financial Year 2018/9 Source: DEFAT, Resources -- Trade Statistics

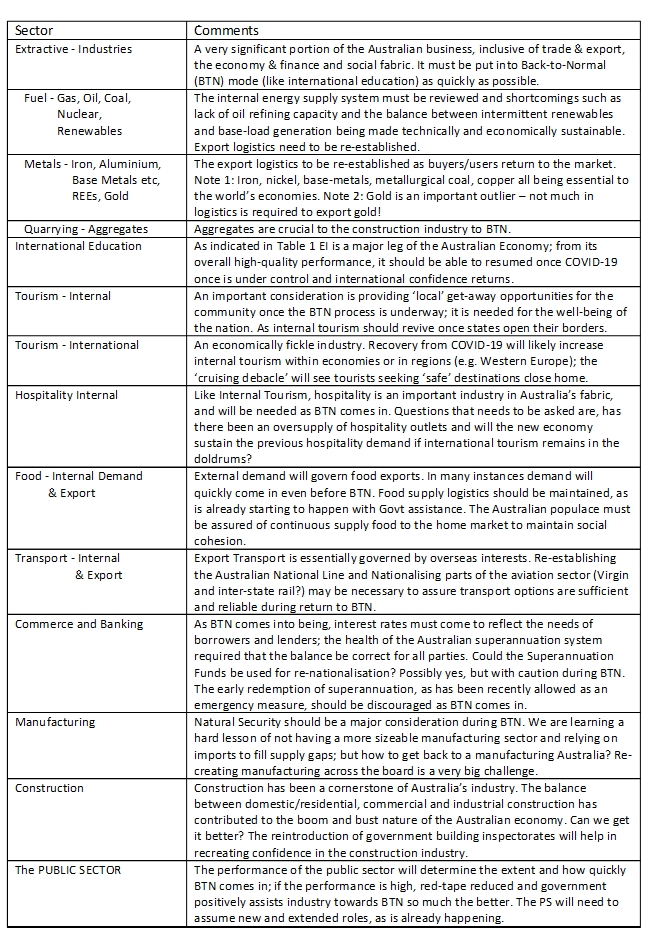

Table 2: Examples of Production Sectors of the Australian Economy

Being the first in que to provide products, raw materials, services and other needs in a Back-to-Normal (BTN) situation; the countries at the head of the que could potentially quickly trade themselves to a BTN; but what is the Normal? Is the Normal the economic and financial situation existed in (enjoyed) prior to December 2019 or is it some new Normal that is yet to be happen.

Table 2 does offer some hints of what a "new" Normal Australia may look like; a country with a smaller services sector, a revitalised manufacturing and industrial sector, a country moving back towards Energy Security, an economy that has an increasingly re-nationalised critical logistics sector, a country carrying a lot of debt (this being in common for all OECD economies), a country with a more realistic educational sector with a revamped technician and trade sub-sector (the reverting of second-tier universities to colleges of advanced education status with the CAEs having strong connections to trades education and training) and hopefully a prosperous EI sector.

The FUTURE NORMAL

Regaining a higher level of independence with respect to energy and fuels (including a realistic balance between renewables and fossil fuels), manufacturing, international logistics (including sea freight), aircraft maintenance, strategic pharmaceutical production, the production of strategic agricultural chemicals and fertilisers, the production of at least moderately transformed manufactures) from raw mined products (e.g. blister copper in place of copper concentrate and moderately enriched uranium instead of yellow-cake, the export of processed food (cold and frozen produce), the maintenance of a better between balance between internal and export food supply, and allowing tourism to recover and re-orientate so as Australia is ready for a steady but increasing flow of overseas visitors whenever the conditions allow. The incentives being offered to employers (e.g. IEs) will assist in recovery; these should be supported by the AusIMM.

The EI Sub-sectors in recovery from COVID-19

Quarrying, the Cinderella of the EIs, needs the construction sector to resume the construction of dwellings, commercial buildings, public infrastructure and "national" projects. The traditional way Australian governments have used to stimulate their economies is to undertake a few selected major infrastructure projects such as the Brisbane cross-river rail tunnel or another runway for Sydney airport; this may not be immediately possible in a post CORVID depressed economy. The construction of dwellings and commercial structures with limited public input but supported by a strong post pandemic recovery private enterprise, will be the best way to support the quarrying industry.

Energy and petroleum must be in consistent supply to the domestic markets. Fossil fuels being natural gas and coal must be available to keep the power grids stable, especially with respect to balancing those energy sources with intermittent renewables. Transport fuel which is principally derived from petroleum must be available such that the strategic inventory is maintained and there is sufficient indigenous useable supply to meet emergency demand; a new Australian refinery that can process petroleum condensate is urgently required for national transport fuel security.

Metals, gold, industrial minerals and uranium are big earners of foreign exchange -- see Table 1. The AusIMM is the professional body that is primarily concerned with the professionals who win and process those minerals. They will be in demand in quantities that were sought up to the end of 2019; they will be in even greater demand from a politically and economically stable supplier like Australia in the future. Their continued production holds a key to lessening the pending financial meltdown (i.e. a depression).

The EIs have a major role in maintaining Australia through this COVID crisis.

To and Fro of the Professional Workforce post COVID-19

There are two counter trends that will become post COVID-19, these are:

- A continuance of the trend for professionals to "migrate" towards to have their share of the benefits of city life that include the proximity to high level health facilities such that the professionals and their families can have fair access to a ICU bed if required, and

- Some professionals will want to leave the urban environments to get away from the post pandemic social challenges that are possible; the observance that many sizeable non-urban communities have little or no COVID occurrences three months into start of the COVID may be important to some as will a ‘relatively’ secure income from some EI operations and will attract urban people.

It is likely that there will be major shifts in the willing and available professional workforce post COVID-19; preparing for this workforce will include long and extensive inductions plus training and education is specific areas of expertise such as mining methodology, ore preparation and logistics systems.

FIFO: a poor solution to the long-term employment challenges of the IEs

Fly-In/Fly-Out is a dangerous employment system for the majority of the workforce; the dangers include economic and logistics factors (e.g. the availability of aircraft/airlines to ferry workers to and from the workplace), health hazards (e.g. flying crews to a site in often smaller aircraft with little space between passengers, the lack of immediate, safe and biologically secure evacuation options, the lack of advanced medical systems in remote sites where the onset of COVID in individuals is rapid) and destruction of social cohesion where family and friends are not available for support in crucial times.

Specific FIFO considerations:

- FIFO for the technicians, lower management and semi-skilled workers: A very risky employment strategy, with long and medium-term downsides as well as immediate risk.

- FIFO for the professional workforce: A means of spreading and sharing professional skills, abilities and knowledge across multiple production sites (and employers in the case of non-tied consultants). The sharing of Professionals for specific areas of industry (e.g. iron ore logistics, gas exploration and aggregate plant engineering) may ease expertise shortages at production sites.

FIFO should be a very restricted and a regulated employment system for the EIs; creating strong links between the workforce and the management of remote EIs is a priority for creating stability.

COVID-19: The Virus -- An Overview

If COVID-19 mutates and produces strains, develops strains that are resistant to vaccines, finds a continuing zoological vector, develops the ability to permanently injure human organs (e.g. the heart, liver and/or kidneys) and/or develops only short-lived immunity post infection, then a seasonal wave of epidemics (like the season flu epidemics) seems likely. Alternatively, COVID may weaken in its transmissibility and in its morbidity, like the Spanish Flu did in the 1920s; this would be a welcome potential happening and would allow medical researchers time to prepare for the next virus and next pandemic. From the published reports, the quest for an effective vaccine is at best estimated to be available in early 2021, however it should be remembered that after 30+years there is still no vaccine for HIV. The search for drugs to mitigate the effects of COVID-19 in infected people is just starting, with or despite President Trump’s support for hydroxychloroquine. The fate of the virus and its effect on our future is largely unknown.

It should be hoped that Government, Medical Research Institutions and Australian Pharmaceutical Corporations continue their work in epidemic avoidance, control and mitigation in the future with an emphasis on national (Australian) biosecurity.

Suggestions for the post COVID Future

- As with all Australian industry be aware of Government incentives to overcome specific challenges, these could be, supporting air transport links and assisting in organising sea transport for minerals and mineral products,

- Using Government guarantees to build up moderate mineral inventories to be available to off-takers at short notice; the Government guarantees are to lessen the potential of product fire-sales,

- Build one or two refineries that can process CONDENSATE; the funding to come from oil and gas producers and explorers, superannuation funds, other Australian industry, the international O&G industries, with direct Government inputs including Defence contributions.

This action should see Condensate Refining Capacity be equivalent to greater than 50% of the projected Condensate output; it will need partial nationalisation of the Australian Liquid Fuels Industry.

- Balancing the LNG exports with local demand for gas, and providing reserve volumes of gas for domestic use,

- Developing coal-to-liquids capabilities for utilising second grade coal and coal washery middlings,

- Using similar CTL plant for manufacturing critical fertilisers and explosives,

- Supporting the installation of LNG Receival Terminals on the Eastern Seaboard of Australia, as has been commenced by AGL.

LNG Receival Terminals on the Eastern Seaboard of Australia, as suggested by Clarke in The Australian Mining Club Journal, September 2004, "Energy security, Business Continuity Management and the terrorist threat" and The US-Australia Energy Dialog, Sydney 2006 and re-emphasised in the paper, "Energy Security for Australia", Clarke and Seddon, AusIMM Bulletin, October 2012.

- Reinvent the Old Commonwealth Employment Service and give it the task of working with the Eis to create a demand in the workforce to be located in remote production sites; initial and concurrent semi-skilled level training and induction will be offered to participants,

- Use Public-Private Partnerships for upgrading rail and other bulk transport systems that will complement the production of the EIs,

- Upgrade the electricity grids; failures in transmission and generation will deepen the recession and reduce the good-will Australia has as a reliable supplier, and

- Over time look at how to get the EIs to move towards producing at least semi-transformed mineral products (e.g. copper matte in place of copper concentrate, enriched uranium from yellow-cake), plus

- Many other opportunities that will become apparent in the medium and long-term.

The Future: Oh, give us a crystal ball that is not too opaque with COVID!

Government assistance CANNOT become an assumed long-term right; financial maturity must be returned to Australia as soon as possible. Industries including the EIs, International Education, Critical Service Industries (e.g. Child Care), Local Manufacturing (inclusive of re-started clothing industries), Shipping and Aircraft Maintenance, Food Production -- Domestic and Export, ... should have some assistance, but must look for long-term independence from Government. The re-nationalisation of key service industries such as electricity, water, waste management, gas, rail, airlines and infrastructure (e.g. roads) should be at least partially achieved, and regulation to insure performance enacted. The national debt will greatly expand, and the currency could devalue, but how will an equitable claw-back of temporary stimuli be accepted by the population?

The EIs Workforce’s Maintenance and Sustenance

Are the EIs up to the costs, OPEX and CAPEX, of maintaining and sustaining their workforce post COVID?

If production can be maintained in remote sites, even at very reduced rates, where moderate stockpiles are allowed to grow, then switching on full production as orders come in should be a relatively simple operation. Letting plant go into a care and maintenance mode reduces OPEX but sees CAPEX rise as the value of worker experience dissipates, this will increase the time and cost to resume full production. If plant is closed down, then costs of getting back to full production will be onerous and restart may be impossible if no experienced workers are available and CAPEX is needed for plant. Companies with deep pockets with possibility of a little from government will be better placed for keeping the production open.

The N in Back to Normal, but what is the new NORMAL?

a. Health; what is known about the long-term health and wellness of the post pandemic population? Also, if a COVID epidemic annual wave becomes part of our existence what will be the human costs of that wave?

As previously discussed, the path that COVID(s) will take is largely unknown; how we defend against the virus, physically live with the virus and how we allow the virus to affect our psyche, is unknown. Also how will the ongoing post virus health of the nation (and world) effect the economic and social recovery?

b. The economies; the world economy, the economies of major trading partners, and the Australian Economy. How long will the recession/depression last? Will international politics become increasingly belligerent because of COVID? What changes will occur that effect our trading partners? Will those changes affect our minerals and fuels export economy, and if so for how long and to what extent?

c. Societal changes to the overall population

It can be assumed that there will be differences between the Pre and Post Recession Workforce. People who have never been unemployed will often not fit back into their previous employment even if it exists post COVID. There will be major changes in lifestyle for many, with many of those changes being from the collapse of incomes. Competition from new school-leavers will affect many unemployed people if the COVID lockdown and subsequent recession lasts for more than two years. The options open to school-leavers will be more restricted in terms of service industries such as hospitality and tourism but may be opened up for working in the EIs and later expanded manufacturing.

The AusIMM: Supporting Critical Industry post COVID

AusIMM is a source of technical knowledge, an entity that represents professionals in its portion of the EIs, a lobbying entity for the EIs with special reference to metals, coal and industrial minerals, a leader amongst the major sectors of the EIs (with other sectors being, petroleum, geoscience, quarrying and environment), and an educational organisation with respect to its abilities in supporting relevant universities (e.g. being an advising entity with respect to curriculum development), but not a professional licensing entity that carries legal risk with respect deleterious actions of its less scrupulous and skilled registrants.

The AusIMM may be able to provide non-prescriptive information on management, general legal, financial affairs and staffing arrangements when questions arising from COVID related factors involve, Force Majeure, Contract Viability and Responsibilities, Legal Liability, Insurance, long-term responsibilities to staff, flexibility on the part of suppliers and logistics providers with respect to government initiatives (e.g. the tenure of sub-contractors and their ability to pay rent)... Here the AusIMM would be a knowledge base to the industry and its professionals.

In Conclusion

We live in interesting times. The COVID pandemic is an example of how civilisation can be challenged with external forces in a very short time. COVID is causing great economic, political and social disruption to a point that a depression is more likely than not. There are opportunities to strengthen the Australian economy as we return to Back-to-Normal life, commerce and the "pursuit of happiness".

Preparation for epidemics that potentially can develop into pandemics has been undertaken since the SARS, MERS and recent Influenzas have become threats. Bird Flu and Swine Flu outbreaks are being monitored as are Measles, TB, Malaria and many other diseases. To be totally prepared for new diseases, vaccines that are effective with multiple viral (and other) pathogens, i.e. that being a vaccine that is effective across a multitude pathogens' types and strains, will need to be developed. Even with such vaccines, great quantities of medical kit will be needed to manage outbreaks and provide protection for frontline responders when a successor to COVID-19 appears; this kit will have limited shelf-lives and be expensive. Note: It is apparent that we are not yet capable of producing very versatile and effective vaccines or making medical kit in the volumes and qualities demanded.

Politically, socially and financially it will be very difficult to put the "Entitlement Genie" back in its bottle; people will make decisions based on the assumption that the $1500 per fortnight, the "job keeper payment", will continue long after its sunset clause of 6 months duration is well past. Their decisions will not be funded post the payments even though many recipients will have resumed some paid work. The national financial situation will need extensive sources of income to stabilise; this will likely need to come initially from the EIs and later a revived manufacturing sector and could be accompanied by inflation and currency devaluation.

Being part of an industry group that is essential to civilisation means that the AusIMM has a role in the economic affairs of Australia. Maintaining the flow of minerals into the world's economies is an important activity during renewal.

Acknowledgements

Irene Ivanova (FAusIMM) and Carlos Sorentino (FAusIMM), being fellow members of the AusIMM Consultants Society and the Membership Retention and Recovery Special Interest Group, are thanked for their contributions to this white paper.

Seminal Comments by Irena and Carlos:

IR1: Value adding to Australian raw industry has long been a missing item. Forced isolation and loss of well-established import chains to Australia may well force us into developing value-added technologies. Australia often dismissed the need to improve the revenues by adding value locally due to low labour costs in China and elsewhere. With the current low Australian dollar combined with comparatively high skilled labour force and high level of unemployment, COVID crisis may well force Australia into developing value added / downstream processing industries. Your paper discusses additional refining capacities but it also leads to locally processed metal ores and concentrate, as well as industrial minerals refining (rare earths?) and delivering much more valuable product to the local market, in turn promoting local manufacturing. As we move to a post-COVID life, this would result in better revenues from higher processed materials export.

Further to that, similar approach could be applied to recycling industries, which presently rely (or should we say have relied) on Chinese reprocessing facilities.

IR2: Australia exports significant number of engineering professionals to the world. These are highly qualified and well regarded. This exit combined with consistently decreasing funding of STEM education in Australia over several years created a negative trend in our professionals. Unfortunately, it is likely that a post-COVID bankrupt government would continue deferring the STEM funding to more pressing economic needs, exacerbating the trend. Using the current lull to upskill the individuals and start engaging them even on part-time basis would potentially be beneficial in the longer run.

IR3: Companies' behaviour and ethics during the COVID crisis may well reshape the post-COVID employment landscape. Whilst the concept of a "job for life" and "ultimate loyalty to an employer" may have been long gone, the approach to the workforce management during COVID may bring some elements of this back. While everyone doing it tough, these companies viewing their workforce as people, attempting to stand down and retain, trying to preserve jobs paying a portion of salary would be ultimately the companies attracting people first. In the post-COVID environment, when the companies compete for skilled workforce (which would always be limited), the behavioural and cultural high grounds would undoubtedly win.

IR4: COVID -19 pushed people into developing skills otherwise unlikely to fully develop or develop fast -- these are working remotely, working from any location (including home or isolated), perfecting use of AV equipment / digital conferencing / digital engagements. This needs to be capitalised upon rather than scaled back post COVID. COVID also highlighted Australian inefficiency in most things Telco -- IT support, broadband, telecommunications; addressing these issues and moving Australian IT to where it needs to be -- on par with US and other developed world should be another important post-COVID task. It will be several times paid by recently acquired digital communication skills, reducing travel, meetings and in some instances rent costs.

CS: At the end of every economic cycle, the economic structure changes and never returns to "normality" that is to say, it never goes back to old patterns of economic activity. If anything is certain is that it will change. How? Nobody really knows.

Author

Dr Mike Clarke, Consulting Engineer, Infrastructure Development & Resource Management, of M.E.T.T.S Pty Ltd, Gold Coast, Queensland

NOTE:

You are welcome to quote up to a maximum of three paragraphs from the above opinion piece, on condition that you include attribution to this website, as follows:

SOURCE: M.E.T.T.S. Pty. Ltd. Website http://www.metts.com.au

M.E.T.T.S. Pty. Ltd. - Consulting Engineers PO Box 843, Helensvale QLD 4212, Australia TEL: (07) 5502 8093 • (Int'l) +61-7-5502 8093 EMAIL: metts[at]metts.com.au Copyright • Privacy • Terms of Use © 1999-2020 M.E.T.T.S. Pty. Ltd. All Rights Reserved. |

.