|

M.E.T.T.S. - Consulting Engineers > White Papers > Coal: Does it have a Future in the Face of the Nuclear Challenge?

Coal: Does it have a Future in the Face of the Nuclear Challenge?

Dr. Michael C. Clarke, CPEng, FIEAust, FAusIMM, RPEQ

Consulting Engineer, Resource & Infrastructure Development

CEO, M.E.T.T.S. Pty. Ltd./Director, Pacific Power Partners LLC

Email: metts[at]]metts.com.au

Share this page:

To the question, does coal have a future in the face of the nuclear challenge, the simple answer is YES! Coal will have a major place in world energy for as long as any of us can foresee into the future. It will only be challenged by nuclear in specific circumstances, and coal has significant advantages over nuclear, as well as alternatives such as hydro and renewables.

Coal’s secure future lies in it unique nature. It is fossilised solar energy, as well as being a complex chemical mixture of carbon and hydrogen (plus a few other elements in minor amounts). Its human face is that it was (and is) the base of our modern industrialised society. To people who have moral objections to our industrialised society, it is greatest curse to ‘natural man’, and now for those same people the hypothesis of anthropogenic caused global warming is the proof of its evil nature. The reality is that coal is the fuel that will continue to power society.

Coal’s applications, in descending magnitude are, power generation, metals smelting (especially iron), cement manufacture, industrial heating (and steam raising), and formerly direct transport fuelling (rail and shipping), and reticulated consumer gas. It will be the source of new liquid transport fuels (produced by Fischer-Tropsch synthesis, direct gasification or as Ultra Clean Coal emulsions, the last being a heavy oil replacement), or as a source of industrial gas where natural gas is not available or is prohibitively expensive.

Coal comes with environmental challenges most of which are related to its constituents. Since good coal consists of greater than 80% carbon, its use will lead to carbon emissions. Burning coal produces carbon dioxide, with around one tonne of coal producing three tonnes of carbon dioxide, plus sulphur oxides (SOx), nitrogen oxides (NOx), and particulates (ROx). In the past it has been a source of significant air pollution, with occasional serious and indeed deadly consequences such as in London in the early 1950s and central Thailand in the 1970s to early 1980s. Recent health concerns that have centered on emissions of mercury and radioactive elements such as thorium and uranium, concerns which are now being addressed.

The human cost of coal is significant. It is believed that thousands are killed in mining accidents each year, in developing Asia and the FSU. Although the emissions from coal utilisation in developed countries have been very greatly reduced and are now at ‘acceptable’ levels, the emissions in the developing world are often at dangerous early industrialisation levels.

Coal faces political challenges. There is a widespread but erroneous political belief that Carbon Dioxide is the chief Greenhouse Gas, and that increases in atmospheric CO2 content are going to cook us. Smog and coal related respiratory diseases have ‘a history’ and are not popular with the voting public even though coal-fuelled power generation in developed countries now has exceptionally low emissions, and lastly Green publicity has promised that we can meet base load power demands with renewables. The move towards introducing an Emissions Trading Scheme is aimed at finding a political fix to what some see as a political embarrassment, i.e. the continuing need for coal in power generation.

Some Coal Facts:

• Coal is an excellent source of raw energy to produce base load electricity (as is nuclear);

• There are hundreds of years of coal reserves in the world;

• Coal is a more democratic fuel that oil, gas or nuclear (Recoverable Coal is distributed of 70+ countries); and

• Developed coal technologies are mature and bankable.

Some Coal and Energy Facts:

• 41% of world electricity is generated from coal (nuclear 15%, gas 20%, hydro 16%. Oil 6% other including renewables < 3%);

• >80% of electricity generated in Australia is from coal;

• New and more efficient coal technologies are coming on line; and

• Coal fired generation is increasing across the world.

More Facts and Figures for Coal and other energy resources:

• Global primary energy grew by 2·4% in 2007;

• Coal was the fastest growing fuel in 2007;

• China which is adding one coal fired power station per week to its grid, is planning to add 1300 GW of capacity by 2030, 70% of which will be coal fired;

• In 2007 World nuclear generation decreased by 2%; although new reactors are coming on line, many existing reactors are approaching the end of their operational lives;

• Growth in World electricity is 5 – 6% pa; and

• The largest growth in electricity consumption will be in the developing world.

From the above dot points, it can be summarised that coal will be with us as a major fuel for power generation for a very long time.

Challenges Facing Coal

Coal does face technical, social and political challenges. The first technical is to be increasingly ‘clean’ and safe, i.e. to be able to meet even more stringent environmental standards. To be able to do this ‘Clean Coal Technologies’ need to be proven, be available for rollout, and be affordable to the developing world in the foreseeable (20 year) future.

If the present political necessity of ‘addressing the Carbon Question’ persists, then large scale Carbon Sequestration (CS) will need to be developed from a concept to a reality. The cost of CS will increase the price of all manufactured products and the cost of services.

The greatest technical challenge for coal is to be ready for meeting the demand for liquid fuels posed by Peak Oil. Technologies for converting coal to oil have been available for over eighty years, but project economics and the inertia of energy planners to major change, has seen Coal-to-Liquids (CTL) languish. (The inertia is also partially economic and comes from proponents having to take a thirty-year view of a CTL project, a time period generally outside a financier’s imagination.)

The social and political challenges are very much involved with public perceptions (partially the result of Green campaigning) and the NIMBY syndrome; they will be awkward to address but with persistence can be resolved.

Meeting the Challenges

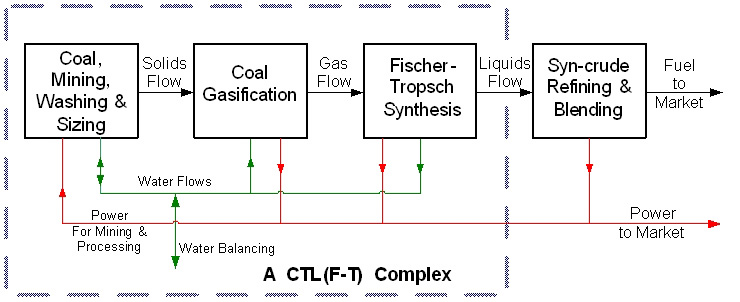

New coal technologies for, power generation, the production of liquid fuels and the replacement or supplementation of natural gas are all required. These technologies are very likely to be based on coal gasification, with one example being CTL based on the Fischer-Tropsch synthesis.

Figure 1. A CTL Complex with Power Generation and Water Management

In Figure 1, coal is gasified thence reacted to form a liquid product. Electricity is produced from waste heat and from the utilisation of a portion of the fuel in a combined cycle power generation plant. If the fuel synthesis portion of the complex is not installed, the gas from the gasifiers can be utilised in a larger power generation operation (an Integrated Gasification Combined Cycle Power Station), or can be reticulated to industry (as a coal gas).

The gasification phase can be a surface operation using coal that has been mined by traditional coal mining techniques, or could be produced by Underground Coal Gasification (UCG), a process that is presently being developed, and one that shows fair promise of success. (Note: Successful UCG can unlock massive coal reserves that are presently unminable due to depth and/or geology.)

The Place of Nuclear Energy and its Challenge to Coal

The nuclear industry has been given new life by the Carbon debate. It is seen by some as the technology that will replace coal as the source of source of base-load electricity. It has a very small waste footprint, a much better record than coal in terms of health and safety, and excellent economics in terms of raw energy cost.

Some Nuclear Facts:

• Australia has around 24% of the world's recoverable uranium;

• Around 50% of the world's recoverable uranium is found in Australia, Canada and Kazakhstan;

• Nuclear resources are NOT very democratic;

• 15% of World electricity is generated from nuclear electricity;

• 24% of electricity in developed countries is nuclear generated;

• There are 440 operating nuclear reactors in 31 countries; and

• To meet 100% of the world base-load demand from nuclear we would need another 1700 large nuclear reactors to displace coal.

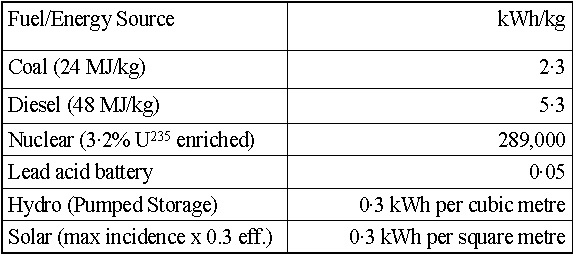

The Energy Density of nuclear fuel greatly surpasses any other fuel, as shown in the table below:

Table 1: Energy Densities

This energy density difference between nuclear and coal results in nuclear having an overall significantly lower physical footprint than coal per unit of power output.

The Dual Nature of Coal and Nuclear

Coal and Nuclear both service the Base-load Electricity Market, and the operation of both types of power stations are similar, in that they are most efficiently operated running at full capacity. Coal and Nuclear Power Stations take time to come on-line from a cold start and are therefore not suitable for meeting peak-load, and only marginally suitable for intermediate-load. Both should have peak and intermediate complementary capacity from natural gas and/or hydro, and both can utilise pumped-storage to assist with peak-load and intermediate-load where the situation allows.

Both groups of technologies require very large capital investment and have long lead-times for planning, construction and commissioning. Coal units that will incorporate oxygen firing and Carbon Sequestration (CS) are expected to have similar capital costs and lead-times to the fourth generation nuclear plants that are also in the planning stage.

Note 1: The cost of CS will be very dependent on the situation of the power station. Where the carbon dioxide can be used for Enhanced Oil Recovery, then there may be some return from its sale to oil producers, as is the case with the N. Dakota Synthetic Natural Gas plant with its sale of CO2 to the Weyburn oilfield operators in Canada.

Note 2: The tendency for new standardised design nuclear plant is to be of very large capacity. The European Pressurised Reactor will be around 1600 MWe, whilst the Westinghouse AP 1000 will be around 1100 MWe. New coal-fired units are often 400 - 600 MWe, with multiple units making up a power station. There is room for nuclear power stations of smaller capacity like the Westinghouse AP 600 (600 MWe) or the South African Pebble Bed at 165 MWe.

Note 3. The price of internationally traded thermal coal has been very fluid, and supply has been tight over 2007/8. In 2009 the price has been weakening and demand marginally lessening. The traded price of uranium has likewise been volatile, however much of the uranium supply has been locked-in with long-term contracts, of $US 70/lb. The prospect for future stable raw fuel prices probably favours coal, since many new resources are planned to come on-line in a number of coal producing countries.

The Relative Cost of Nuclear and Coal Fired Electricity

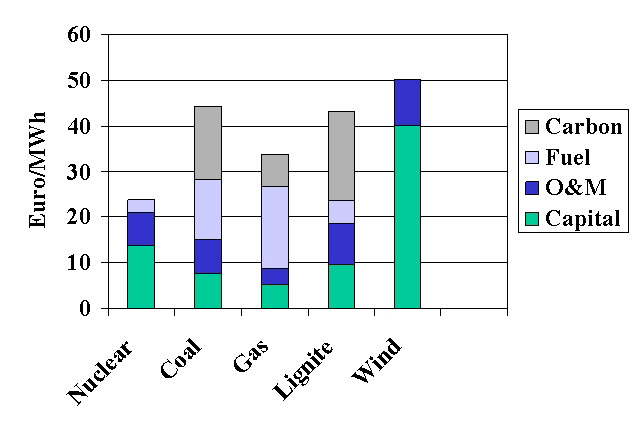

Figure 2. Comparative Electricity Costs. After Tarjanne & Lucstarinen 2003.

The figures in the above graph, are based on a European scenario, and therefore indicate a high price for imported coal. The nuclear fuel price includes an allowance for decommissioning. The Wind energy capital cost includes the cost of stand-by fossil fuel units and wind plant redundancy.

Comparative Nuclear and Coal Plant Operation

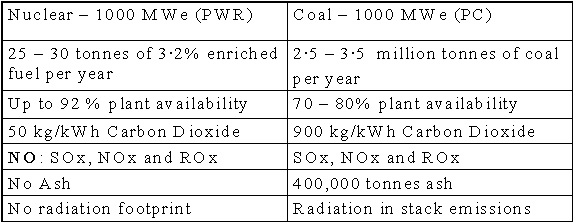

Table 2. A Comparison for 1000 MWe Power Stations

Notes on Table 2.

1. The respective power stations have the same power capacity, but the nuclear plant would produce around 23% more electricity than the coal plant, due to the coal plant’s higher maintenance requirements,

2. The nuclear plant would produce around 25 – 30 tonnes of High Level Waste per year. If this waste were reprocessed, that waste tonnage would be greatly reduced.

3. The radiation footprint of a coal-fired power station is produced by its emissions of Thorium and Uranium that are minor constituents of coal.

The Australian Fuels Situation

Australian power generation is dominated by very cheap, abundant and dedicated black coal.

In Victoria, South Australia and Western Australia there is even cheaper lignite for power generation. The cost of producing electricity in Australia is one of the lowest in the world thanks to well developed coal and lignite resources. The Australian electricity industry has cheap options for ash disposal from coal combustion, very convenient coal/lignite logistics in Eastern Australia, natural gas at below international prices for meeting peak-load and access to hydro for meeting peak and intermediate loads.

Future Australian Coal Exploitation and Power Generation

Coal will continue its base load dominance, whilst natural gas will increase in its share, especially for peak and intermediate load, and if Australia goes into Coal-to-Liquids, some new base, intermediate and peak generation will be derived from co-generation in the CTL complexes. UCG may provide a means of accessing deep coal, but open-cut and underground mining will continue to supply coal for power generation, smelting and cement manufacture in the foreseeable future.

The Nuclear Industry

Australia has no indigenous nuclear fuels industry and no nuclear power industry. It mines uranium ore and turns it into yellowcake. Nuclear fuels and nuclear power research stopped in Australia around forty years ago.

Nuclear power generation in Australia is not likely to be introduced in the near future with the possible exception of small dedicated nuclear plants for water desalination, with these plants being South African designed Pebble Bed units.

In terms of the world situation there will be no significant impact of nuclear power on coal fired generation in the near term future. Nuclear energy (power production) currently has a long lead-time for installation caused by, the lack of experienced and qualified vendors of internationally acceptable nuclear plant, the existence of big gaps in the skills base in nuclear engineering, reticence by some nations to depend on a raw energy with a very narrow supply base (and questions of national sovereignty re nuclear plant inspections), and project bankability concerns given the examples of nuclear plant cancellations because of political intervention in the past.

Nuclear plant fabrication capacity in the West will be taken up by orders for replacement units for the United States, United Kingdom, France, other European countries and later Japan and Korea. China, India and Brazil will be building nuclear power stations for themselves, but they will have limited capacity to export technology. These capacity constraints could take two decades to resolve for nuclear energy.

(Similar restraints in production can be expected for new coal power stations that incorporate the latest technologies. There are a limited number of vendors who can fabricate and install major state-of-the-art coal fired units, whilst there is also a shortage of engineers and technicians to carry out the projects. These capacity constraints could take at least a decade to resolve for coal.)

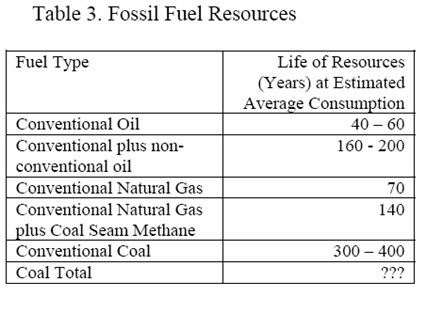

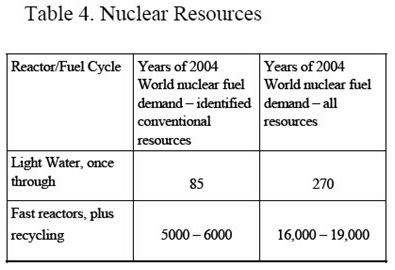

Fuel Resources

Much has been stated about Peak Oil, and there is some opinion that the World has already ‘passed peak oil’. If so, there will be developing a desperate need for supplementing and replacing traditional oil resources. CTL will be one option that will be looked to. On the nuclear side, the use of nuclear energy to produce liquid fuels appears to be limited to liquefied or compressed hydrogen production. The widespread use of liquefied or compressed hydrogen as a transport fuel is not a certainty for the future, given the unresolved storage and transport challenges for hydrogen.

Coal and nuclear raw fuels have huge untapped resources. The coal resource is still being understood, with non-conventional (deep and geologically challenging) resources only now being considered. Nuclear Resources (Uranium and Thorium) went through a hiatus in exploration and development from the 1970s to the end of the twentieth century. The good news is that although the resources are not yet fully defined, they are very extensive.

(Tables 3 and 4: After IAEA Nuclear Technology Review 2005)

For coal, if non-conventional coal is considered (this includes lignite, deep coal, and carbonaceous shale), the resource is huge and not able to be estimated given the lack of knowledge. With natural gas, methane hydrates are not considered in Table 3.

For nuclear resources, the 85 years of fuel resources for Light Water Reactors on a once through system, takes into account the availability of U235 in resources that are mineable at the present price of uranium. If recycling of fuel is considered, the fuel available jumps by two orders of magnitude.

In terms of resources, the good news is that we have vast amounts of coal and raw nuclear fuels.

Conclusion

Nuclear energy cannot knock coal of its pedestal of being the world’s premier raw energy source for the production of electricity. In some developed countries, the percentage of nuclear power in their energy mix could approach that of France (~80%) over the next forty years. Coal will continue to be dominant in iron smelting and in cement manufacture. Coal could also be the source of a major portion of liquid transport fuels in the next thirty years.

Coal technologies for power generation and conversion to liquids will continue to improve, whilst mitigating environmental consequences of coal use will be a feature of coal developments. Coal mining must become safer in the Third World, whilst the introduction of UCG (if technically successful) will offer new levels of worker safety in coal extraction across the world.

Sources

Asian Development Bank

Australian Greenhouse Office

BP World Energy Statistical Review

International Atomic Energy Authority

International Energy Authority

World Coal Institute

World Energy Council

World Nuclear Organisation

NOTE:

You are welcome to quote up to a maximum of three paragraphs from the above white paper, on condition that you include attribution to this website, as follows:

SOURCE: M.E.T.T.S. Pty. Ltd. Website http://www.metts.com.au

Share this page:

Author: Michael C Clarke

(Michael C Clarke on Google+)

M.E.T.T.S. Pty. Ltd. - Consulting Engineers PO Box 843, Helensvale QLD 4212, Australia TEL: (07) 5502 8093 • (Int'l) +61-7-5502 8093 EMAIL: metts[at]metts.com.au Copyright • Privacy • Terms of Use © 1999-2014 M.E.T.T.S. Pty. Ltd. All Rights Reserved. |

.